What:

A largecap fund with a targeted method

Why:

- Props up returns by taking tactical calls

- Comprises downsides and delivers over the long run

Whom:

Average threat traders with a long-term view

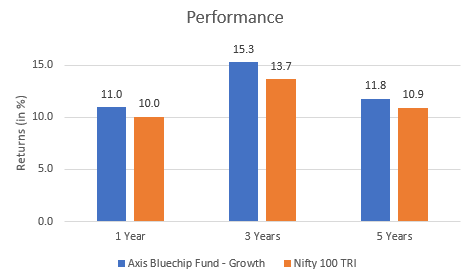

Axis Bluechip (beforehand referred to as Axis Fairness) delivered 12.8% returns within the final 5 years towards 12% delivered by benchmark index Nifty 100 TRI. At a time when largecap funds have been struggling to outperform the benchmark, the fund’s concentrated method and dynamic calls have given it an higher hand. The fund has seen ups and downs, extended streaks of underperformance and durations of flashy returns. However what stands out is its long-term efficiency. Regardless of durations of underperformance, the fund nonetheless scores on long run metrics. Current adjustments in its technique have helped enhance returns tremendously.

Change in technique

After sustained underperformance from 2016 to most of 2017, the fund has recovered. It has been progressively morphing right into a concentrated fund from being a comparatively diversified fund. There have been adjustments in majorly three facets:

- Focus – The fund at the moment has a portfolio of 23 shares with the highest 5 holdings contributing to over 40% of the portfolio. The portfolio has shrunk by half from 3 years in the past. HDFC Financial institution is its high holding with a close to 10% publicity. Three years in the past, the inventory was nonetheless high holding however with an publicity of round 8%. Regardless that the fund wasn’t categorised as a targeted fund, its technique follows a targeted method with excessive conviction bets.

- Asset allocation – The fund has decreased midcaps and upped its debt publicity. From late 2016 until 2018, the fund has been reserving out of midcaps. In the course of the robust midcap rally in 2017, the fund was decreasing publicity. From publicity of 14% originally of that yr, the fund introduced it right down to 7% by Jan 2018. Funds like SBI Bluechip and ABSL Frontline Fairness held round 14% in midcaps throughout this era. This is likely one of the the reason why its efficiency paled subsequent to its friends. Nonetheless, it benefitted when the rally ended as a result of it was reserving income by means of the highs. The fund additionally started taking money calls and began rising money from early 2018. The fund held as much as 18% in debt in early 2019 in comparison with a gradual publicity of 1-3% until 2016. This primarily decreased the general threat of the fund.

- Tactical Strategy – The fund turned extra tactical in its method, deftly shifting out and in of shares. Publish-2017, its portfolio turnover virtually tripled from ranges of 50-60% to 150-180% exhibiting its change in technique. For instance, it began reserving income in Maruti Suzuki in early 2018 when the inventory was at its peak. And since then, progressively decreased publicity there. The place it noticed potential, it managed to time the entry effectively. TCS and Bajaj Finance are such shares the place the fund started climbing exposures in early 2018 and caught the rally. Even the place shares had been held for a very long time, the fund usually booked income and made contemporary entries.

Portfolio

{kind=link}

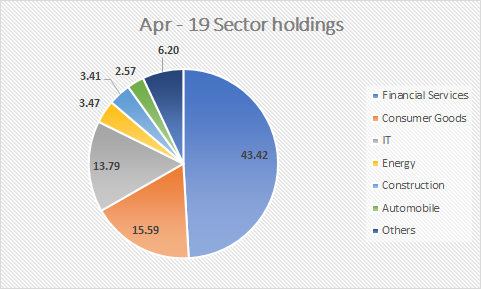

The fund’s portfolio has benefited from the slim rally now we have been seeing. It has over 40% publicity to banking and monetary providers whereas having very small exposures to auto and vitality shares which have fallen out of favour. The fund deftly modified exposures to completely different sectors and shares whereas reserving income throughout rallies and averaging out prices throughout slumps. The fund took proper sector calls, be it selecting up IT or regular pruning of auto publicity in early 2018. It additionally benefited from the FMCG rally in 2018 the place it at all times maintained a very good publicity.

It additionally ventured into newer shares by taking part in IPOs, however was fast to let go if it didn’t see the potential. SBI Life Insurance coverage and HDFC Life Insurance coverage had been held for all of two months put up their itemizing. Quite the opposite, the fund purchased into Avenue Supermarts put up the IPO and has been rising publicity.

Efficiency

Largecaps as a class have largely been trailing the index. Within the final 5 years, primarily based on 1-year rolling returns, funds have crushed Nifty 100 TRI solely 43% of the time. Axis Bluechip has managed to outperform the index 70% of the time, solely subsequent to Mirae Asset Massive cap. Regardless that the fund went by means of durations of underperformance, it made up for it. If we take a look at longer-term returns, 3 and 5 years, the fund nonetheless beats the benchmark.

Returns as of 1st July 2019.

Regardless of the fund taking concentrated calls and having a excessive portfolio turnover, it’s comparatively much less risky. Commonplace deviation, a measure of volatility, is decrease than the class common. This aids the fund in producing higher risk-adjusted returns. Based mostly on rolling 1-year returns during the last 5 years, the Sharpe ratio of the fund is second greatest amongst its friends.

The fund additionally incorporates downsides significantly better than different funds within the class. Taking a look at 1-month returns for the final 5 years, the draw back seize ratio stood at 89%, worse than solely 2 funds. This attribute may also be noticed from how the fund carried out in several market cycles. Since its launch in 2010, markets noticed two main declines – in 2011 and 2015. The fund misplaced lesser than the class in each situations.

Axis Bluechip is appropriate for average threat traders in search of long run choices (5 years or extra). It may be used to construct core portfolios as it would lend stability. The fund is managed by Shreyash Devalkar since Nov 2016 and has an AUM of ₹5,144 crore.

Different articles chances are you’ll like

Publish Views:

6,083