Picture supply: Getty Photos

With markets at document highs — even within the often sluggish FTSE 100 — it may be difficult to seek out high quality development shares buying and selling at cheap valuations. Nevertheless, I believe these two match the invoice, and will due to this fact be value interested by for a Shares and Shares ISA.

Uber

First up is Uber Applied sciences (NYSE: UBER). Hardly per week goes by with out me utilizing its app for taxis or meals delivered. I lately booked prepare tickets on there for a visit to London and acquired 10% off a experience on the different finish.

On the finish of December, there have been 171m energetic month-to-month customers (14% greater than the 12 months earlier than). Gross bookings grew 18% in This autumn (or 21% at fixed forex charges), serving to income leap 20% to $12bn.

Whereas development is nothing out of the bizarre for Uber, what’s new is the corporate’s profitability. It has gone from incinerating billions a 12 months to producing practically $7bn in free money circulation final 12 months. Income are anticipated to go a lot increased in future.

Star hedge fund supervisor Invoice Ackman lately took a large $2bn stake within the inventory. He has a wonderful observe document of recognizing high-quality companies that show to be undervalued.

Ackman stated: “We consider that Uber is among the greatest managed and highest high quality companies on the planet. Remarkably, it could possibly nonetheless be bought at a large low cost to its intrinsic worth.”

The inventory’s buying and selling at a ahead price-to-earnings (P/E) a number of of 30, which is affordable for a market chief rising the underside line very strongly.

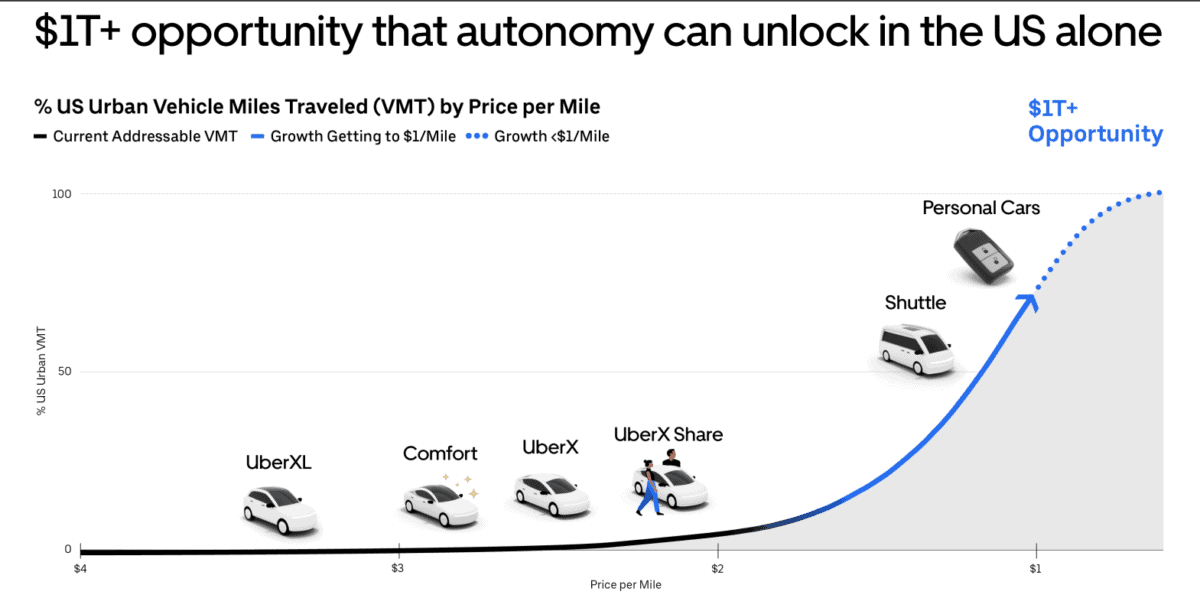

What may go improper? Properly, if self-driving taxis from Waymo and Tesla ever develop into mainstream, Uber’s driver-based mannequin may very well be disrupted. It is a real long-term threat, assuming these deep-pocketed companies construct their very own networks.

That stated, Uber has partnered with a number of main autonomous automobile (AV) corporations, spying a $1trn+ market alternative within the US alone. The considering is that if AVs finally drive down the per-mile price as a result of there are not any drivers to pay, each bookings and Uber’s earnings may explode increased.

Ashtead Know-how

The second inventory is AIM-listed Ashtead Know-how (LSE: AT.). It is a firm that rents out specialist subsea rental gear to the worldwide offshore vitality business. That features each renewables (wind generators) and oil and gasoline.

Fuelled by an acquisition-driven development technique, income soared 52% to £168m final 12 months, with underlying working revenue coming in increased than anticipated at £46.6m. The compound annual development fee in earnings over the previous 5 years stands at 41%.

Within the buying and selling replace for 2024, CEO Allan Pirie stated: “With one of many largest and most technologically superior rental fleets within the business and a continued give attention to operational excellence, we stay assured within the Group’s capability to generate substantial long-term worth for shareholders.”

Dangers right here embrace financial downturns or world vitality worth shocks, which may sluggish exploration and decrease demand for rented gear. The agency’s additionally a small-cap valued at £426m, so doesn’t have the monetary firepower of a agency like Uber.

Nonetheless, I like the chance/reward set-up right here. The share worth is down 33% in six months, leaving the inventory on a low ahead P/E ratio of 11.6. At 531p, I believe the inventory may very well be a hidden gem and is worthy of additional analysis.